Although only 20,000 jobs were created in February, as the U.S. draws closer towards full employment, the best economic metric to look for in the coming months will be rising wages throughout most employment sectors.

Virginia's Public Square

Virginia's Public Square

Although only 20,000 jobs were created in February, as the U.S. draws closer towards full employment, the best economic metric to look for in the coming months will be rising wages throughout most employment sectors.

While GDP may be slowing, what Americans really need are wage increases.

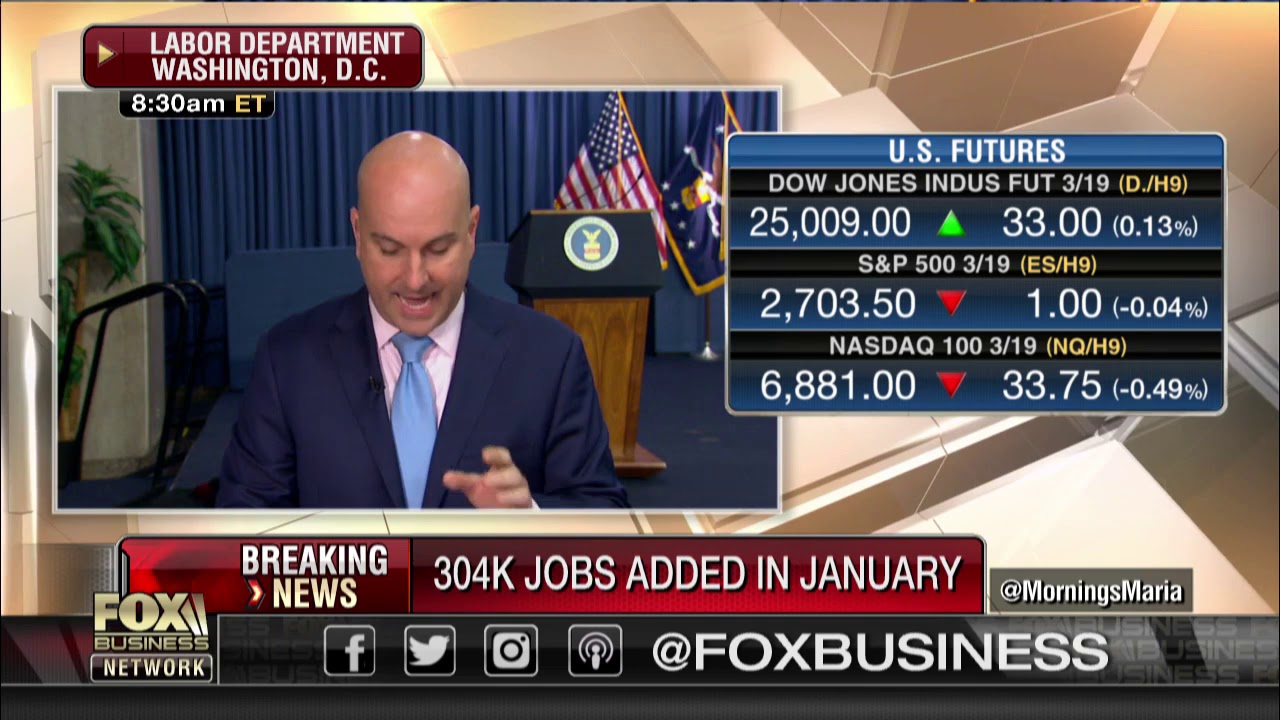

Despite a 35-day partial government shutdown that affected over 800,000 federal employees, the January jobs report absolutely shattered expectations. The U.S. Labor Department reports that non-farm payrolls surged by 304,000 last month.

Private sector payrolls were up by 296,000, with big increases seen in the construction and leisure and hospitality industries.

The unemployment rate, however, did tick up 0.1 percentage point to four percent, largely as a result of the longest government shutdown in U.S. history. Regardless, January was the 11th consecutive month that the unemployment rate has been at or below four percent.

According to a report from CNBC, economists had expected payrolls to rise by 170,000 and the unemployment rate to hold steady at 3.9 percent.

Although the economy is said by many market analysts to be slowing down, the month of January marked 100 months in a row of positive job creation, the longest streak on record.

There were two big corrections that were made for previous month’s numbers. December’s gain of 312,000 jobs was knocked down to 222,000, the largest revision since November 2014. Meanwhile, November’s job gains were hiked from 176,000 to 196,000. The corrections brought the three-month average to 241,000, still trending well in U.S. economic expansion.

For the full year of 2018, the average monthly jobs gain was 223,000.

Even though the number of Americans employed slid down to 156,694,000 from 156,945,000, the U.S. labor force participation rate is now at 63.2 percent, the highest under President Donald Trump.

The U-6 metric, a figure used to measure unemployment that takes into account discouraged workers and those holding part-time positions for economic reasons did rise to 8.1 percent from 7.6 percent, on track with January 2018.

The Labor Department also reported that average hourly earnings rose by 3.2 percent year-over-year in January – the sixth month in a row above three percent. Average weekly earnings fared better, rising 3.5 percent year-over-year.

“As the jobs and employment data normalizes over the coming months, we are confident the nation’s economy will continue to build on the strength seen in 2018 and the first report of 2019,” said Labor Secretary Alexander Acosta.

Following increased market volatility and the slowing of global growth at the end of last year, the Federal Reserve is set to take a less aggressive approach to interest rate hikes in 2019 after the U.S. central bank instituted four rate increases in 2018.

The Federal Reserve Bank of Atlanta forecasts GDP growth at 4.1 percent in Q3 as chairman of the U.S. central bank Jerome Powell said at a conference that more economic growth is in store after half century-low jobless claims and a target goal of two percent inflation.

With the unemployment rate at an 18-year low and jobless claims at a 50-year low, the U.S. economy shows no signs of slowing down anytime soon.

Ending a big trading week on Wall Street, investors are anticipating great news from the Q2 GDP report, the economic scorecard for the U.S.

For Democrats running on the economy for the 2018 midterm elections, claiming the “crumbs” that came with the Tax Cuts and Jobs Act à la Nancy Pelosi have not helped Americans, jobless claims are in for last week, and Americans receiving unemployment aid has dropped to the lowest number since March 1973.